There is no doubt that the senior housing market is encountering some changes. Despite these changes experts agree that market fundamentals remain strong. Population demographics including an age wave that is set to boom in the coming two decades, present an undeniable opportunity for growth.

Recently, the senior housing and care market is looking at historically low occupancy. The last two years were undoubtedly a time of challenge for senior housing owners and operators. Two main factors to this include, a decline in occupancy nationwide, and an ongoing staffing crisis for providers.

The upside to this is that investors, now have the ability to acquire these buildings, skilled nursing facilities, assisted living facilities and independent living facilities, at a relatively low price per bed.

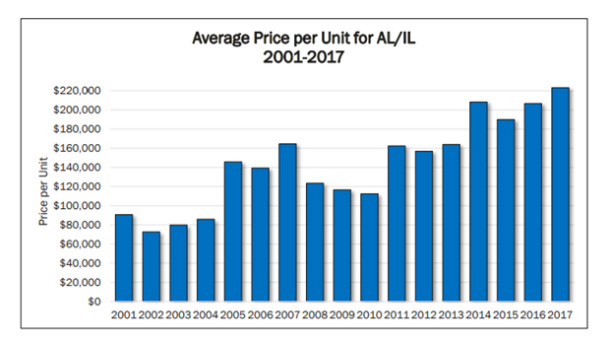

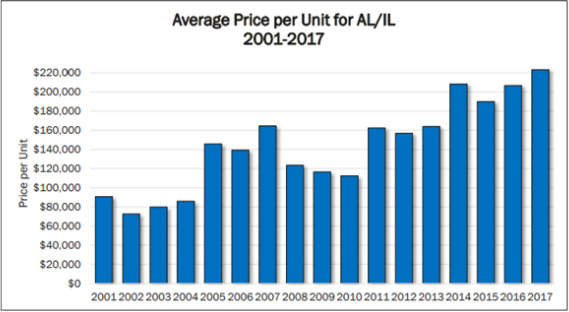

During the three years leading up to the great recession the senior housing market was unprecedentedly strong. This was followed by a three-year lull including 2010, which produced the lowest value per unit despite it representing the year the market began to turn around. The market more than made up for this lag in 2011 when the average price per unit surged by 44{ab00da231405656ab53e236adbc822260719de0342a41ff7a037e7d07eabcb24}.

It took another three years where the average price stayed in a tight range before the next surge in pricing occurred jumping another 27{ab00da231405656ab53e236adbc822260719de0342a41ff7a037e7d07eabcb24}. The abundance of new developments that broke ground in 2014 and 2015 opened their doors in or around 2017 driving a competitive scramble for more than just residents. Not only did this put pressure on unit pricing, it also effected the already scarce labor, resulting in higher labor costs and increased turnover.

Sources:

(2018). SENIORS HOUSING AND HEALTH CARE MERGERS & ACQUISITIONS IN THE 21ST CENTURY (4th ed.). Norwalk, CT: Eleanor B. Meredith.

Approximately 43.5 million caregivers have provided unpaid care to an adult or child in the last 12 months, and about 34.2 million Americans have provided unpaid care to an adult age 50 or older in the last 12 months National Alliance for Caregiving and AARP. (2015). Caregiving in the U.S.] 15.7 million of those adult family caregivers care for someone who has Alzheimer’s disease or other dementia. The value of services provided by informal caregivers has steadily increased over the last decade, with an estimated economic value of $470 billion in 2013, up from $450 billion in 2009 and $375 billion in 2007.

Approximately 43.5 million caregivers have provided unpaid care to an adult or child in the last 12 months, and about 34.2 million Americans have provided unpaid care to an adult age 50 or older in the last 12 months National Alliance for Caregiving and AARP. (2015). Caregiving in the U.S.] 15.7 million of those adult family caregivers care for someone who has Alzheimer’s disease or other dementia. The value of services provided by informal caregivers has steadily increased over the last decade, with an estimated economic value of $470 billion in 2013, up from $450 billion in 2009 and $375 billion in 2007.

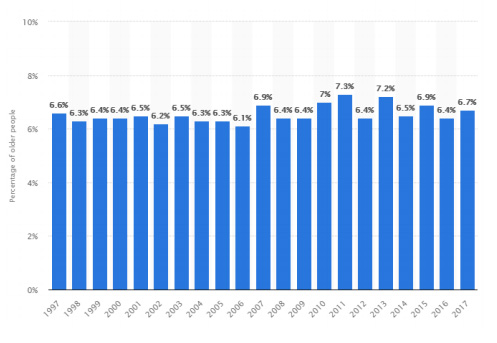

The first of the boomers — the population born between 1946 and 1964 — turned 65 in 2011, and the last will turn 65 in 2029. By 2030, boomers over 65 will make up 20 percent of the U.S. population, numbering around 60 million people, according to a

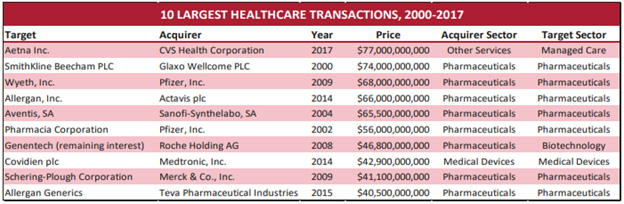

The first of the boomers — the population born between 1946 and 1964 — turned 65 in 2011, and the last will turn 65 in 2029. By 2030, boomers over 65 will make up 20 percent of the U.S. population, numbering around 60 million people, according to a  In the managed care sector, that showed itself in the attempt by four of the largest health insurers to merge into two companies in 2015. The combined dollar value was $91.2 billion. They were both challenged in the courts and both were terminated. By 2017 and 2018, a new mega-merger trend emerged, with CVS announcing a proposed acquisition of Aetna for $77.0 billion after Aetna’s attempt to buy Humana for $37.0 billion was terminated. Then it was Cigna’s turn, announcing its intent to purchase Express Scripts for $67.0 billion, after its purchase by Anthem for $54.2 billion was terminated. These companies are trying to re-write the healthcare delivery market, and we suspect there will be more to come.

In the managed care sector, that showed itself in the attempt by four of the largest health insurers to merge into two companies in 2015. The combined dollar value was $91.2 billion. They were both challenged in the courts and both were terminated. By 2017 and 2018, a new mega-merger trend emerged, with CVS announcing a proposed acquisition of Aetna for $77.0 billion after Aetna’s attempt to buy Humana for $37.0 billion was terminated. Then it was Cigna’s turn, announcing its intent to purchase Express Scripts for $67.0 billion, after its purchase by Anthem for $54.2 billion was terminated. These companies are trying to re-write the healthcare delivery market, and we suspect there will be more to come.